What is a mortgage anyway? If you are thinking of buying a home, you might be asking yourself this simple question.

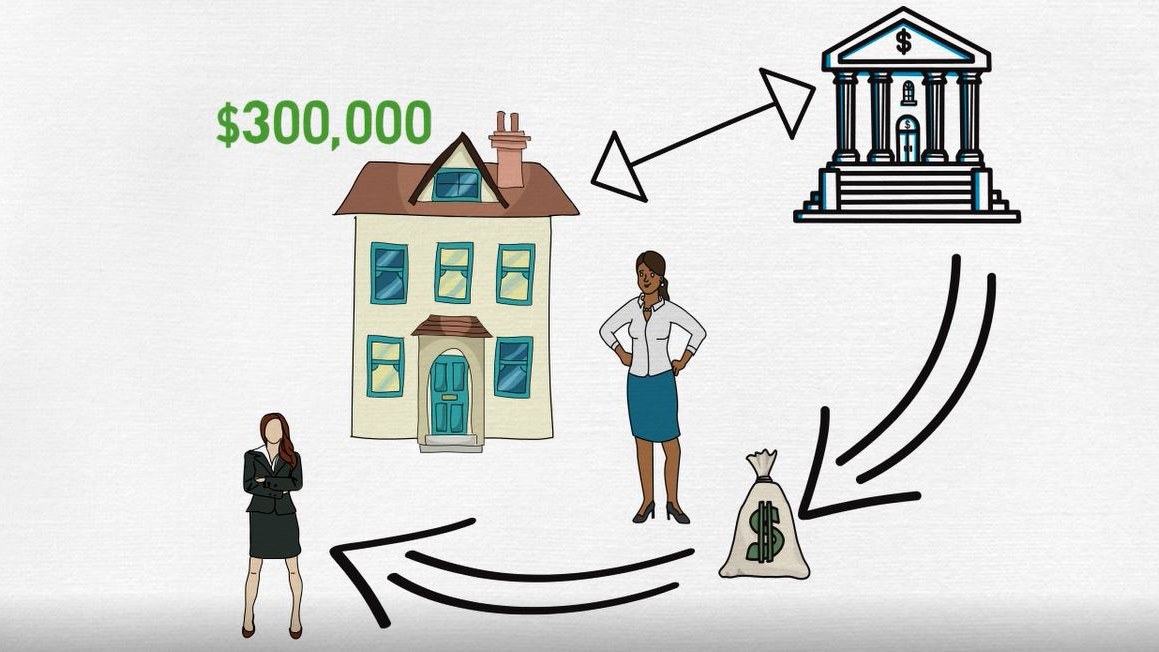

If you’re buying a home with a price of $300,000, you have two options. The first is to pay cash. In other words, use $300,000 of your savings to pay the person selling the home. Most home buyers simply don’t have enough in savings to cover the full price of the home they’re purchasing, so they need to take out a loan to pay the seller.

A mortgage is a type of loan that is tied to the home you are buying. If you sell that same home down the road and there is a mortgage tied to it, the bank gets paid before you do. Or if you stop making your monthly payments, the bank can take your home, through a process called foreclosure, to recoup the money they have loaned to you.

Tip

There is an important point to remember when buying a home with a mortgage. You’re shopping for two main things. First, you’re buying the actual home. Second, you’re also buying a loan. That loan—the mortgage—has a price tag, just as the house has a price tag.

You’re buying the money that you’re borrowing in the form of a mortgage, and it’s important to shop for the best value, just as you shop for the best value in a home. You should compare current mortgage rates.

The amount you borrow is the principal or loan amount. This amount goes to the seller, along with your down payment, to cover the price of the home. Deciding on the right home price is an important decision you will need to make.

In addition to paying back the loan amount, you must also pay interest and possibly fees, points, and mortgage insurance.

All that can seem very confusing, so it’s best to add all the costs of the mortgage together when comparing one lender with another. Two of the most important things that will affect the cost of your mortgage are the home price and the mortgage term.

A higher home price will require a higher loan amount, which will result in more interest that you will have to pay your bank.

You pay back the loan amount to the bank over the term of your loan. This term is typically 30 years. Choosing a shorter loan term, say 15 years, will result in a higher monthly payment. A 15 year loan will lower the cost of your mortgage. This is because you are paying interest for half of the amount of time.

Next, we’ll talk about your down payment.