The monthly payment on a 700k mortgage is $5,180.

You can buy a $778k house with a $78k down payment and a $700k mortgage.

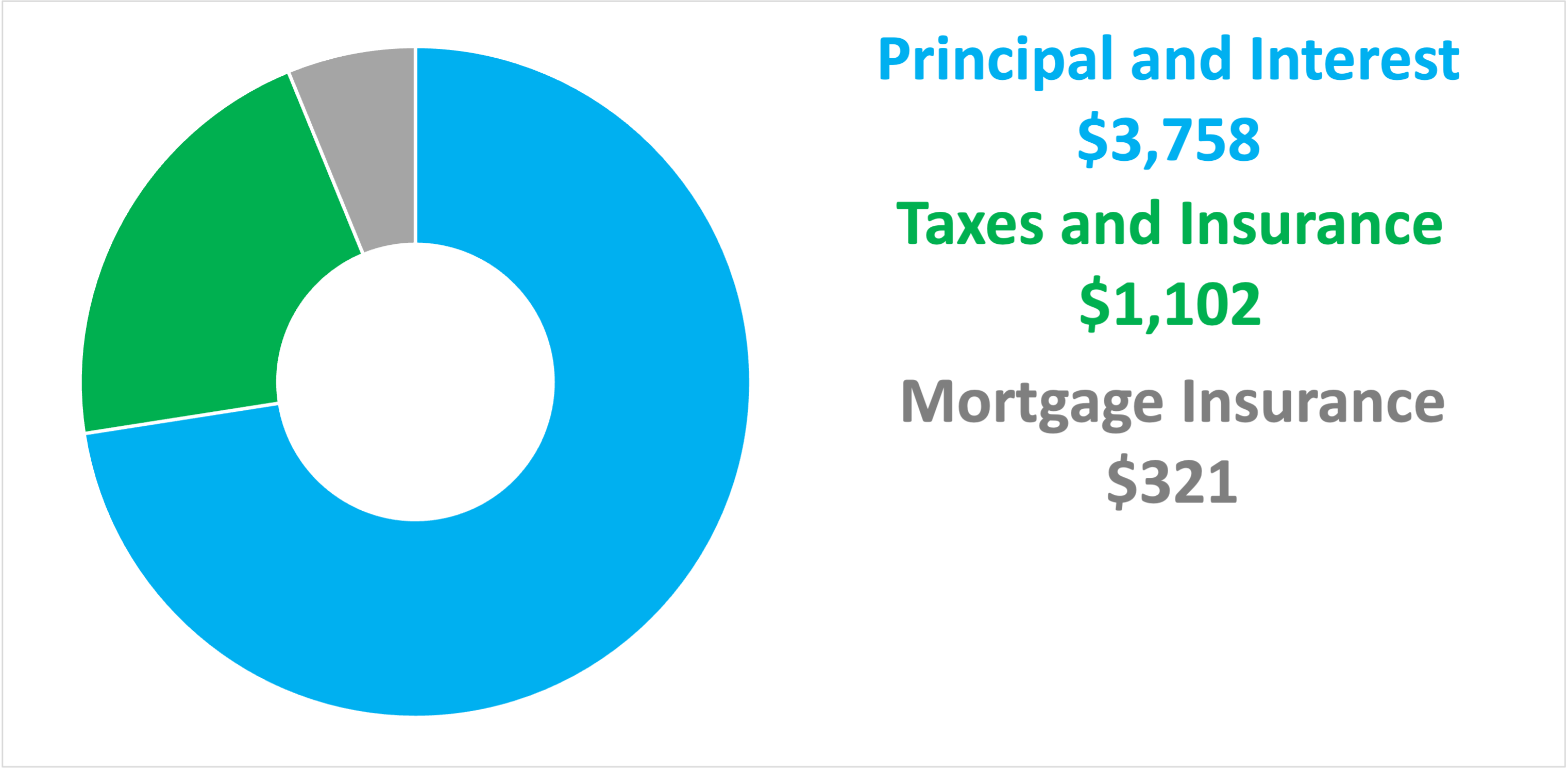

Monthly Mortgage Payment

Your mortgage payment for a $778k house will be $5,180. This is based on a 5% interest rate and a 10% down payment ($78k). This includes estimated property taxes, hazard insurance, and mortgage insurance premiums.

If you want to change some assumptions, try out our simple mortgage calculator.

Income Needed for a 700k Mortgage

You need to make $259,022 a year to afford a 700k mortgage. We base the income you need on a 700k mortgage on a payment that is 24% of your monthly income. In your case, your monthly income should be about $21,585.

You may want to be a little more conservative or a little more aggressive. You’ll be able to change this in our how much house can I afford calculator.

Take the Quiz

Use this fun quiz to find out how much house I can afford. It only takes a few minutes and you’ll be able to review a personalized evaluation at the end.

We’ll make sure you aren’t overextending your budget. You’ll also have a comfortable amount in your bank account after you buy your home.

Don’t Overextend Your Budget

Banks and real estate agents make more money when you buy a more expensive home. Most of the time, banks will pre-approve you for the most that you can possibly afford. Right out of the gate, before you start touring homes, your budget will be stretched to the max.

It’s important to make sure that you are comfortable with your monthly payment and the amount of money you’ll have left in your bank account after you buy your home.

Compare Mortgage Rates

Make sure you compare mortgage rates before you apply for a mortgage loan. Comparing 3 lenders can save you thousands of dollars in the first few years of your mortgage. You can compare mortgage rates on Bundle

You can see current mortgage rates or see how mortgage rates today have trended over last few years on Bundle. We monitor daily mortgage rates, trends, and discount points for 15 year and 30 year mortgage products.

What Determines How Much House You Can Afford?

- Your credit score is an important part of the mortgage process. If you have a high credit score, you’ll have a better chance of getting a approved. Lenders will be more comfortable giving you a mortgage payment that is a larger portion of your monthly income.

- Homeowners association fees (HOA fees) can impact your home buying power. If you choose a home that has high association fees, this means you’ll need to choose a lower priced home to in order to decrease the principal and interest payment enough to give room for the HOA dues.

- Your other debt payments can impact your home budget. If you have low (or zero) other loan payments you can afford to go a little higher on your mortgage payment. If you have large monthly obligations for other loans such as car payments, student loans, or credit cards, you’ll need to back off your monthly mortgage payment a little to make sure you have the budget to pay all your bills.

How much will you need for a down payment?

A long time ago, you needed to make a 20% down payment to afford a home. Now, there are many mortgage products that allow you to make a much smaller down payment. Here are the down payment requirements for popular mortgage products.

- Conventional loans require a 5% down payment. Some first time homebuyer programs allow 3% down payments. Two examples are Home Ready and Home Possible.

- FHA loans require a 3.5% down payment. In order to qualify for an FHA loan, the property you are buying must be your primary residence.

- VA loans require a 0% down payment. Active and retired military personnel may be eligible for a VA loan.

- USDA loans require a 0% down payment. These are mortgages that are available in rural areas of the country.

What are the steps to buying a home?

- Play around with a few mortgage calculators. Start getting comfortable with all the costs associated with buying a home. Many people are shocked when they find out how much extra property taxes and homeowners insurance adds to their payment every month.

- Check your credit score. Many banks will now show you your credit score for free. You can also use an app like credit karma.

- Get pre-approved. Sometimes the seller will require an upfront security deposit or a due diligence fee just to get a signed purchase agreement. If you get declined for a mortgage, you might lose this money.

- Start searching for a home online. Use redfin or zillow to narrow down your choices and make sure you like the homes in your price range.

- Decide if you want to use a real estate agent. Remember, that your agent gets paid by splitting the commission with the seller’s agent. Sometimes you can get a better deal by negotiating or choosing to buy your home without an agent.

These are the most important pieces to getting approved

- Your credit score. Ideally, you want this to be above 700, but there are mortgages that only requires a 580 credit score.

- Your monthly income. This is the main limiting factor on how much you can afford. Take your annual income before taxes and multiply it by 3 or 4. This is a good starting point.

- Your cash to close. Make sure you have enough cash to close and a little buffer. The required cash to close is typically 5-10% of the home price and includes your down payment, escrow, and fees that you’ll pay for a closing attorney, title search, and appraisal.